According to much research, about 65% of the general population are visual learners, and providing visuals along with data improves both comprehension and retention. So, adding a dashboard or snapshot summary as the cover page for the more detailed financial report packet, featuring charts and graphs showing trends and comparatives, is likely to enhance understanding among your board members and other key stakeholders of your organization’s financial data.

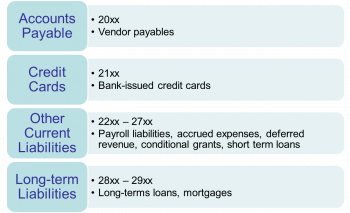

Liability accounts reflect what you owe to others and what you hold on others’ behalf. For small and midsize nonprofits without overly complex systems, 4-digit account numbers are usually adequate. Longer numbers can certainly be used, but that requires more keystrokes and may be harder to remember. Liability account numbering usually begins with 2.

Assets accounts reflect what you have (cash, investments, fixed assets), what others might owe to you (receivables, deposits), or what you might have invested for the future (prepaids, inventories). For small and midsize nonprofits without overly complex systems, 4-digit account numbers are usually adequate. Longer numbers can certainly be used, but that requires more keystrokes and may be harder to remember. Assets account numbering usually begins with 1.

An all-volunteer national advocacy effort to increase financial sustainability among nonprofits through building and maintaining operating reserve funds.

Mission

To define, promote, and facilitate the practice of building and maintaining operating reserves throughout the nonprofit sector as a key strategy toward ensuring the long-term sustainability of the organizations and programs that save and enhance our lives.

Finance committees are also often charged with ensuring compliance and/or developing other policies that further serve to protect the organization and manage its exposure to risk. These include establishing policies for:

Finance Committee responsibilities relating to reporting and monitoring include:

1. Develop useful and readable report formats with staff. 2. Work with staff to develop a list of desired reports noting the level of detail, frequency, deadlines, and recipients of these reports. 3. Work with staff to understand the implications of the reports. 4. Present the financial reports and communicate the implications to the full board. 5. Monitor cash flow and ensure adequate resources are available for day-to-day operations (working capital) and mission accomplishment.