About Us

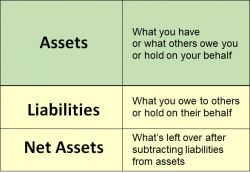

Assets

The Statement of Financial Position (SOFP) is the correct nonprofit term for the balance sheet. The SOFP comprises three sections: assets, liabilities, and net assets.

Assets are usually listed in order of declining liquidity. Current assets are those available as cash or equivalent within one year. Longer-term assets are those to be used or that are receivable over one year such as multi-year pledges, long-term investments, and fixed assets. Following are examples of what typically comprises assets for small and midsize organizations.

What you have:

• Cash in bank accounts, investment accounts, petty cash, and change funds

• Things your organization has bought for future use, such as merchandise inventories or supplies

• Payments your organization has made for goods or services that have not yet been received or used such as annual insurance premiums that could be refunded to you if cancelled, or expenses relating to future fiscal years paid in advance (prepaid expenses)

• Fixed assets such as furniture, equipment, and improvements to your facility, listed at cost, that are non-liquid, as the cash has already been spent to acquire them

• Accumulated Depreciation, a “contra asset” (against asset) indicating the extent the fixed asset has decreased in value as it is used up (depreciated) over its useful life

• Collections of art, artifacts, other valuables related to your mission

• Long-term investments of unrestricted or temporarily restricted funds

• Long-term investments of permanently restricted principal such as endowment funds that cannot be used for operations

What is owed to you:

• Grant awards promised to your organization but not yet received

• Revenue earned from services provided by your organization for which payment has not yet been received

• Loans your organization may have made to others

What is held by others on your behalf:

• Deposits your organization has paid to others and is held by them such as advance rent, utilities security deposits, payroll bonds, etc.

Assets are a natural “debit balance” meaning that, in an accounting entry, a debit to an asset account will increase it. A negative number (credit balance) in the assets section of a balance sheet is unusual and should be questioned and explained, except for Accumulated Depreciation. As noted above, Accumulated Depreciation is a “contra asset” (against asset) account that tracks the depletion of the value of fixed assets as they are used.

Below are questions you might want to ask when looking at the asset balances to ensure that resources are being deployed effectively and efficiently and per plan. This information is most helpful in trend, so looking at it in comparison to one or two previous fiscal years will help provide more context for your analysis of the data.

The answers to these questions, along with the answers pertaining to other balance sheet sections, will provide a better understanding of the organization’s financial position.

Return to the Internal Reports Introduction page for links to greater detail on how to read various reports as well as recommended formatting.