Nonprofit Accounting Basics

Internal Reports Introduction

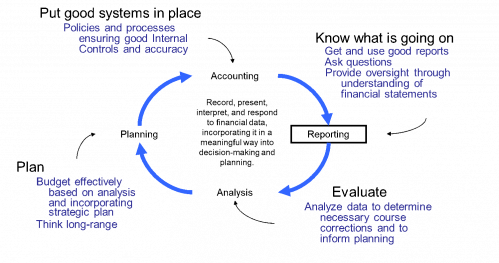

Reporting is a key component of the Financial Management Cycle.

Think of your reports as your chief communications tool to inform stakeholders about what’s going on with your organization financially. Good internal reports are accurate, timely, and readable. They present relevant financial information, with enough context (numeric data, comparisons, projections, and narrative) to promote a thorough understanding of your status, how closely you are following your budget plan, and what actions may need to be taken.

You often hear that “numbers by themselves don’t mean very much,” for good reason. So be kind to your readers. Provide comparatives and do the math for them. Anticipate their questions and provide what you think they should know and focus on.

About the Statement of Activities (aka Profit & Loss, income and expense report, or budget report):

• What is the annual budget for this year?

• What was last year’s total?

• How do we expect to end the current year and how does that compare to the approved budget?

• What are the reasons for (any) significant variances?

• What is the status of restricted donations, if any?

• What is the call to action that results from reading the report? That is, what needs to be done to recover from a grant being declined or an increase in program demand?

About the Statement of Financial Position (aka Balance Sheet):

• Do we have enough cash to pay our bills?

• Have we borrowed from the Operating Reserve or the Line of Credit? When can they be repaid?

• Are receivables or payables around the same as usual? (If different, narrative notes should explain why.)

• Are there sufficient liquid assets to cover the net assets with restrictions?

• What portion of net assets is available for operations versus restricted by donors or invested in property, plant, and equipment?

Staff and board can agree in advance on which reports to produce, what they will look like, who will get them, and how often. This inventory of regular reports should minimally include: the Statement of Financial Position (SOFP) and the Statement of Activities (SOA). For the general board, these could be one-page summary reports with narrative notes, supplemented with specific focus detail reports as needed. Detail reports might home in on cash flow projections, fundraising progress, and individual programs, projects, or events.

No matter how small the organization, high-quality financial reports lead to better financial management.