About Us

Budgeting for Capital and Financial Goals

What’s necessary to achieve a stable, healthy, mission-driven nonprofit? And how can we budget for adequate financial flexibility? An organizational budget includes both the annual operating revenue and expenses as well as a capital budget, or capitalization plan, ensuring resources for future fixed asset and long-lived and/or non-operating needs.

A capital budget might cover several years and include target amounts and fundraising strategies to achieve strategic and financial sustainability goals. These could include:

- Asset purchases (such as equipment, facility acquisition, or leasehold improvements)

- Asset investments (such as inventory purchases or production costs of a product the organization will sell)

- Financial stability targets (such as building an operating reserve, reducing loan principal, or eliminating a deficit)

- Strategic targets (such as building a fund to support program or management initiatives per its strategic plan)

Capital budgets often require a funding plan separate from and in addition to the operating budget. An organization’s capital budget is different from a capital campaign budget, which is usually for bricks-and-mortar or other finite projects.

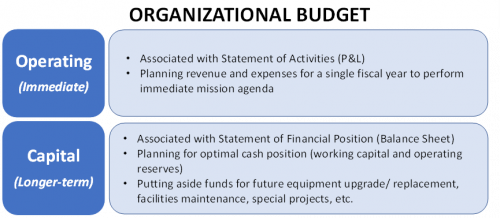

An organization's operating budget reflects its planned financial activities for a single fiscal year, showing how much revenue it expects from which sources and how much it will spend on operations. A capital budget, or capitalization plan, relates more to an organization's financial position: its assets, liabilities, and net assets, setting forth goals and targets for these areas.

Although the concept may seem odd for a small or midsize nonprofit organization to consider, the truth is that all organizations have a capital structure, whether they are actively aware of it or not. Good financial management requires an organization to be aware of and intentional about its capital structure – the balance among its assets, liabilities, and net assets. An organization is encouraged to determine what its own financially healthy balance might look like, and to plan (i.e., budget) toward financial goals that will help it to achieve, and maintain, that balance. Creating a capital budget, or capitalization plan, in tandem with its operating budget, will help to ensure that the organization has a full understanding of immediate and longer-term cash needs, encompassing both operating and nonoperating components.

The following articles contain more details on the following elements of budgeting for capital and setting capital structure targets: Operating Reserves; Deficit Reduction; Debt; Furniture, Equipment, and Technology; Facilities; Special Funds; and Endowments.

Return to the Budgeting & Financial Planning Introduction page for links to a sample “4-Year Capital Budget Costs & Funding Sources” and other content and downloadable resources pertaining to budgeting.