About Us

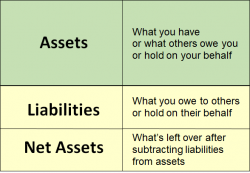

Net Assets

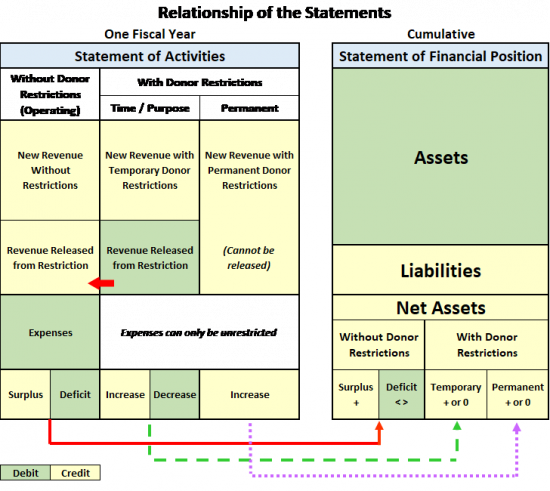

The Statement of Financial Position (SOFP) is the correct nonprofit term for the balance sheet. The SOFP comprises three sections:assets, liabilities, and net assets.

Generally accepted accounting principles (GAAP) call for an organization’s net assets to be classified as “with” or “without” donor restrictions. Net assets were formerly presented as unrestricted, temporarily restricted, or permanently restricted. Organizations should track the financial transactions related to all donor restricted gifts in the accounting records to determine the status of the organization's use of the gift and for reporting purposes.

Small and midsize nonprofit organizations typically do not have net assets that are restricted permanently, such as endowments, and it is usually not advisable for them to do so. Having an endowment ties up cash that is not accessible to the organization for operations or program delivery. It is far more advisable for small and midsize nonprofits to build working capital cash and to fund an operating reserve before attempting to create an endowment. If a small or midsize nonprofit does have an endowment, the donor often requires that the income generated from the gift be used for operations or for a specific purpose. While a separate cash or investment account does not need to be established, the accounting records should include a calculation and entries to showing how this restriction has been met.

Net assets are the cumulative result of all the years of an organization’s fiscal activity. The relationship between the statement of position and the statement of activities is shown below:

Net assets may include contributions received or promised to the organization that carry a donor-imposed restriction as to when (time restriction) or for what purpose (purpose restriction) the gift can be used, or a restriction requiring that the funds be set aside permanently, often allowing the income earned on the amount to be used for operating purposes or for a specific purpose as noted above. If donor restricted net assets are not fully released during the year the gift was received, the balance is carried over to the subsequent fiscal year are and shown as net assets with donor restrictions. All net assets that are not restricted (without donor restrictions) can be used by the organization as its board sees fit.

It is useful for internal financial management purposes, and for disclosure requirements if an audit is conducted, to separate liquid from non-liquid assets to show the organization’s liquidity more clearly, lifting out the financial resources it can use for day-to-day transactions for a given period of time. However, if the organization has accepted a gift restricted by the donor, it has agreed to honor the restrictions. In cases where the gift must be used for a specific program(s) or set aside permanently, the liquidity calculation should be adjusted to reflect the amount needed to appropriately release restrictions during the period being analyzed.

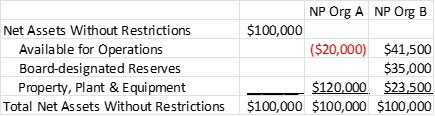

Further, providing a single lump sum balance for net assets without donor restrictions often does not tell the full story. For instance, the total net asset balance in all three examples below is $100,000.

If shown in one lump sum, as in the first column, where only the total for net assets without restriction is showing, it would be easy to assume that the organization was in decent shape with a positive $100,000 in net assets without restriction. But that presentation would be masking a liquidity problem for Nonprofit Org A. And Org B, with the same total, tells a completely different story, as it distinguishes between available vs. designated vs. the non-liquid (fixed) portion of net assets.

With more detailed information as to the composition of net assets, different conclusions about these organizations’ financial health would be reached. The breakdown for Org A shows it has spent all its available cash on equipment or its facility and has an accumulated operating deficit of $20,000. Org B’s presentation shows it has planned for financial stability by maintaining operating cash and setting aside reserve funds in addition to investing in some equipment. Showing the net assets in this greater detail would help Org A’s board to understand why the organization has positive net assets but is still struggling to pay the bills on time.

The objective is to present clear and easily readable reports, and not to make the reader work hard to figure it out. Accounting for and reporting net assets in these more detailed categories for internal reports is valuable and recommended and gives a clearer picture of the organization’s actual financial position for the board and other stakeholders.

See also: Reclassifying Net Assets in QuickBooks

Return to the Internal Reports Introduction page for links to greater detail on how to read various reports as well as recommended formatting.