About Us

Budgeting Approaches - Revenue

The budget process was described earlier in the Budgeting section as the way an organization goes about building its budget. In this, the second of a four-part series on good budgeting approaches, we discuss budgeting for revenue, with an emphasis on contributions.

Practice revenue-based budgeting.

Budgeting is a form of risk management, and the most reliable budgets yielding the best fiscal results for the organization are conservative and revenue based. This means:

• Budget for revenue first. Base revenue targets on realistic expectations and only include reasonably reliable (perhaps 70%+ likelihood) revenue in the budget. Never include a revenue projection that simply fills the gap to cover expenses. This sets the organization up for a budget deficit if the organization fails to hit the "plugged" revenue targets.

• Take care to understand the impact and timing of donor restricted contributions and releases on the operating budget.

• Ensure expenses are lower than the dependable revenue total. This requires cooperation among all departments in assessing programmatic effectiveness, setting organizational and programmatic priorities, and timing new or adventurous programs.

Analyze and understand your revenue concentrations.

Might your organization be overly dependent on single source of revenue? In some cases, lack of diversification of revenue sources could pose a serious risk to the financial stability of an organization should a single large revenue source become unavailable. But this may not always be true. There is no universally right mix of revenue sources - the right mix for your organization depends on your particular circumstances, your mission, your industry, your staff capacity, and even the age of your organization.

• For an organization with little or no earned revenue associated with programs, having 80% of revenue from government sources may make total sense because of reliable, ongoing contracted programming.

• For another organization, whose revenue sources appear to be well distributed among earned, government, foundations, corporations and individuals, the realization that 90% of foundation revenue comes from one large grant from a single foundation may still pose a concentration risk.

• Risk may also be present if a big portion of an organization's annual revenue depends on the success of a single fundraising event or annual program event. The organization must understand the impact a cancellation of the event would have and whether there is a way to mitigate the risk.

An organization’s mix of revenue sources will naturally change over time, so it is a good idea to regularly step back and reflect on funding strategies. Lean toward what is now working best while also considering new opportunities.

Be intentional about how resources are applied.

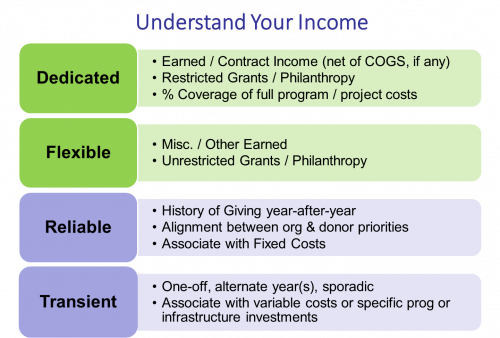

Some revenue sources are dedicated to certain activities and are used to cover those related expenses. Earned revenue in the form of ticket or merchandise sales, tuition, entry fees, contracted services support the specific related program activities. Donors can also restrict their funding to support certain activities that align with their philanthropic focus areas.

Flexible, unrestricted revenue is the most desirable. Even better if it is reliable from year-to-year. Such revenue can be used to cover unavoidable/ fixed costs. Transient funding is a bit more difficult to predict and manage. Apply transient funding to controllable costs to create if-then scenarios to prepare for these funding uncertainties.

As noted in the Budgeting Process section of this website, budgeting for revenue is best done when board, staff, and stakeholders are appropriately involved, and when the approach to budgeting is disciplined, informed, and intentional.

Return to the Budgeting & Financial Planning Introduction page for other content and downloadable resources pertaining to budgeting.

© 2023 Elizabeth Hamilton Foley