About Us

Activity-based Budgeting-An Internal Organization Approach

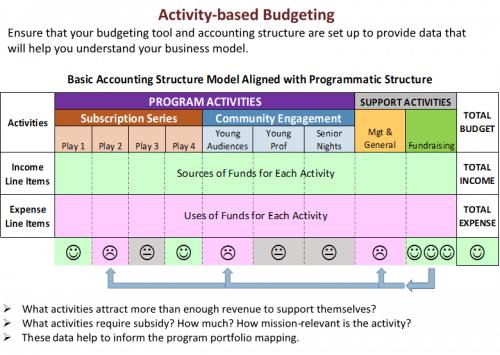

Once the mix of programs has been confirmed during the preparation phase of budgeting, activity-based budgeting is a way to show how the organization plans to allocate resources to the mission and support (functional) activities of the organization (programs, management, and fundraising).

Activity-based budgeting shows your organization’s business model. It relates dedicated revenue to full expenses for each activity, clearly showing how much subsidy from unrestricted funds (assigned to the Fundraising effort) is needed to support the activity. Full costs include each activity’s share of direct and indirect or common costs that are fundamental to implementing the activity. Ensure that your budgeting tool and accounting structure are set up to provide data that will help you understand your business model.

External reporting requires an organization to assign expenses to program, management, and fundraising activity classes to comply with GAAP and IRS requirements. The model above, showing both revenue and expenses by activity, is only for internal reporting, to assist in program portfolio analysis and to provide information that may be useful to developing fundraising strategies.