About Us

Accrual vs. Cash

Accrual accounting – and budgeting – matches revenue and related expenses in the same fiscal period, regardless of the timing of the receipt or disbursement of actual cash. Many small and midsize nonprofit organizations operate on a modified accrual basis – that is, mostly on a cash basis except for year-end adjustments for accrual. See the “Basic Accrual Concepts” page in the Budgeting section of this website for a discussion of seven basic accrual concepts and how they affect budgeting for small and midsize organizations.

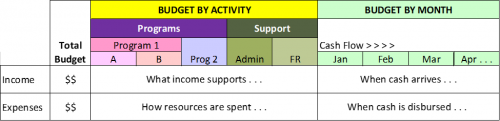

Even though you’re budgeting on an accrual basis, having a section of the budget that estimates month-over-month timing for receipts and disbursements of budgeted line-item totals will assist with predicting cash flow and developing year-end budget projections. As noted in the “Internal Reports” section of this website, cash flow and year end projections are both important components of good management reports.