Accounting and Bookkeeping

Reclassing Net Assets in QuickBooks

QuickBooks (QB) is a very reasonably priced accounting solution used by many small and midsized nonprofit organizations. One drawback, however, is that it does not have a way to separate net assets on the balance sheet other than by past or current. It starts with three “equity” (net assets) accounts:

- Opening Balance Equity – a utility account that is used only for setting up a new company in QB. After setup, this balance should remain at zero.

- Net Income – shows the current year net income derived from all income and expense accounts, regardless of donor restriction.

- Retained Earnings – an account into which all prior year net activity is accumulated, regardless of donor restriction. QB transfers current year net income into Retained Earnings as of the last day of each fiscal year, so the Net Income “account” can begin showing the new current year activity.

As nonprofits, we are required to show our net assets “with donor restrictions” (restricted) separately from those “without donor restrictions” (unrestricted). In addition, we may want to make further distinctions within our unrestricted net assets to delineate board-designated funds (operating reserves or other special purpose reserve funds), or to show non-liquid net assets such as net equity in property, plant, and equipment (PP&E) (value of net fixed assets less any related long-term debt). These further distinctions are not required by GAAP (generally accepted accounting principles), but they provide more clarity for management and internal understanding of net assets composition and liquidity. QuickBooks software is good, but it cannot do this breakdown for us.

The Workaround

In order to split net income and retained earnings into the net asset accounts appropriate for our purposes, we need a little work-around. This can be done via journal entry at the end of each fiscal year. To prepare this entry, you will need to determine what the new ending balances need to be.

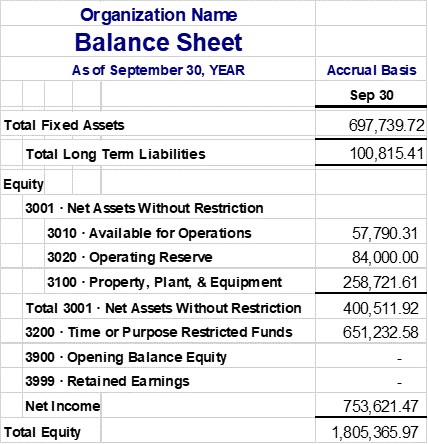

Your first step will be to export a year-end Balance Sheet from QB to Excel, customized to include “all rows.”

Then you will hide all the asset accounts except for “Total Fixed Assets,” and you will hide all the Liability accounts except any “Long-term Liability” that is related to any of the fixed assets, such as a vehicle loan or a mortgage. It should end up looking something like this:

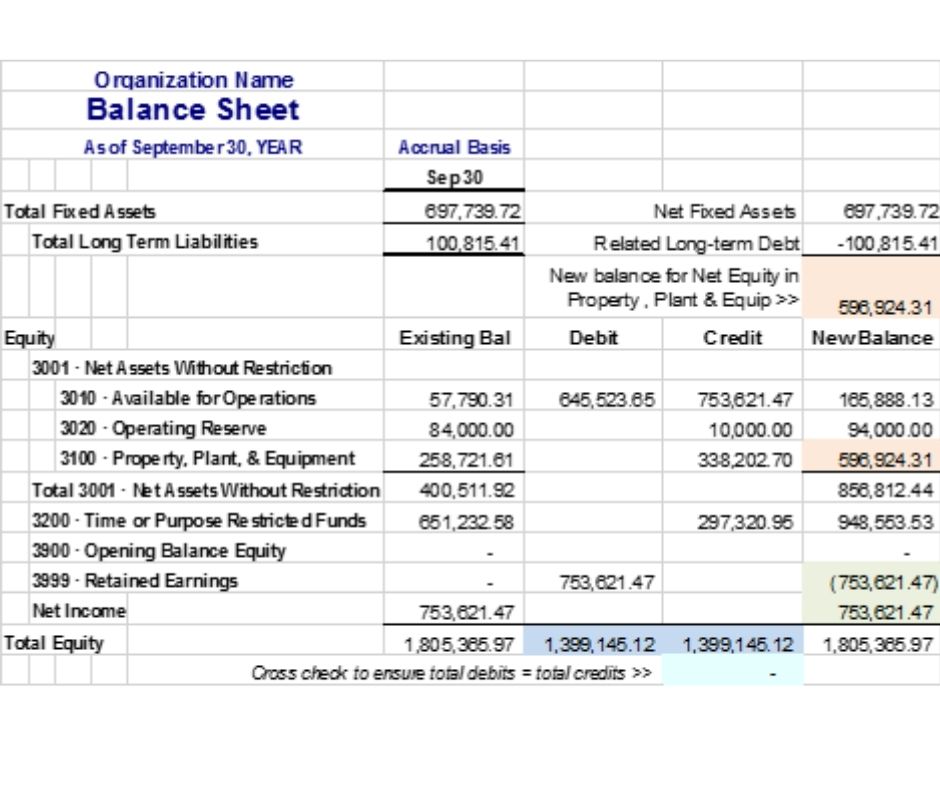

Next you will need to add some columns and rows and do some calculating to determine the debits and credits that get you to the desired new balances for your “internal” net asset accounts. In the example below, the board designated an additional $10,000 to the Operating Reserve since there was a larger than normal operating surplus. In addition, there was a capital project campaign (to renovate program space), and several large campaign contributions were not fully spent on the project by year-end. Some funds that were spent on the project increased the value of net fixed assets.

Below is an illustration of the analysis needed to update the internal net asset balances to the correct amounts. Columns are added to the right of the “Existing” balance columns to show debits, credits, and the new balance for each line item. Net Assets have a “natural” credit balance, so a credit to a net asset account will increase the balance, and a debit to that account will decrease it.

Enter a formula for each line item (not subtotals) in the “New Balance” column:

=Existing Bal <less Debit> + Credit.

Create formulas to total the Debit and Credit columns to ensure they are equal.

A cross-check formula subtracting total credits from total debits should equal zero.

Note that the Total Equity in the “Existing” column and in the “New Balance” column will also need to be equal, once all the debits and credits have been entered. This whole process is done to reclass among the equity accounts – it should not change the overall total. Here is what’s happening:

- The illustration shows that $10,000 will be added to the Operating Reserve. This increase is done by crediting the Reserve account.

- The PP&E balance will increase by $338,202.70, an amount determined by calculating the difference between the existing PP&E balance and the new PP&E balance (orange highlight). Since the new balance is higher, this will be a credit; if it were lower than the existing balance, it would be a debit to the PPE account.

- The Restricted balance will increase by $297,320.95, an amount determined by calculating the difference between the Existing Restricted total and the New Balance for Restricted. The amount credited here reflects the “change in net assets” within restricted activity; a reduction would be a debit. This net restricted activity amount should be available from your P&L (and/or your restricted tracking schedule), which should show the net change resulting from increases and releases during the fiscal year.

In order to make these adjustments possible, the simplest way is to first transfer the Net Income total to the Available for Operations (AFO) account before making the other adjustments. This is done by debiting or crediting Retained Earnings (RE) by an amount equal to the opposite of Net Income. That is, if Net Income is positive (a credit balance), RE will be debited for that amount and AFO will be credited. If Net Income is negative (a debit balance), RE will be credited and AFO will be debited. Together RE + Net Income should = zero (green highlight).

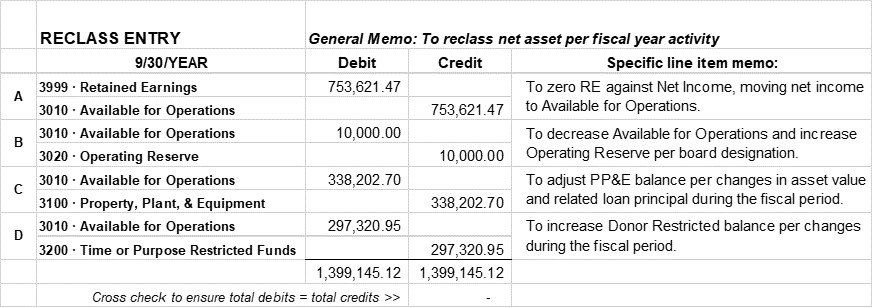

The following illustration shows the series of balanced entries that accomplish the “workaround” reclass of net assets for our example at fiscal year-end:

The Retained Earnings account should only be used once per year to reclass at fiscal year closing, since that is when QB converts the fiscal year’s net income to retained earnings. You may get a warning pop-up message from QB that you are changing a proprietary account. You can override this if you have done the preparation and feel confident about the adjusting entries. (Tip: Back up QB before making the entry.) Always double check the balance sheet to ensure that the RE and Net Income together = zero at year-end, and that the internal account balances match the New Balance columns as expected, to prove that the entry was done correctly.

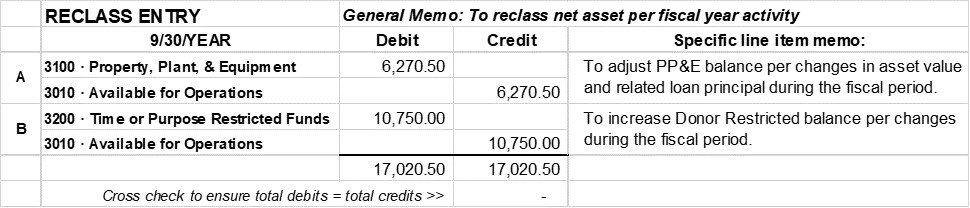

To show interim (monthly or quarterly) changes to the Reserve, PP&E, or Restricted net assets balances, debits and credits would be made among the “internal” accounts only and would not include any changes to the RE account. For instance, the following month, if the change in PP&E for depreciation expense was $6,270.50, and $10,750 was released from restriction, the interim reclass entry would look like this:

The debit to the PP&E account reduces the account balance per depreciation. The debit to the Restricted account reduces the account balance by the amount that was released from restriction. For the interim report, the Net Income to-date (from QB) would be counted with the amount in Available for Operations to get the unrestricted (net assets without restriction) total.

Using this workaround, you can use QuickBooks to its best advantage and still be able show net assets balances that are appropriate for your organization.

© 2021 Elizabeth Hamilton Foley

See also Internal Reports.