Nonprofit Accounting Basics

Subrecipient Monitoring: Essential Information for Successful Implementation

Federal funds often flow through multiple organizations before being used to aid the intended beneficiary. The organization receiving federal funds from another organization, rather than directly from the federal government, is referred to as the subrecipient. The organization sending the funds is referred to as the ‘pass-through’ organization.

Many reasons exist that require the use of subrecipients, similar to how federal award grantees hire vendors, contractors, and consultants. Depending on the size and complexity of the federal award, several layers of subrecipients may be required. Some of the more typical reasons include:

- Expertise: Subrecipients may have specialized expertise or resources that the grantee does not have and can bring those resources to the program.

- Geographical Reach: Subrecipients may be located in areas where the grantee does not have a presence, which can help expand the reach of the program.

- Efficiency: By delegating certain responsibilities to subrecipients, the grantee can focus on other aspects of the program, which can lead to greater efficiency.

- Capacity: In some cases, the grantee may not have the capacity to carry out the program on its own, and subrecipients can help fill that gap.

Contractor Versus Subrecipient

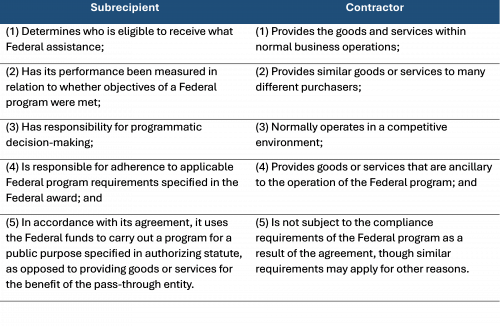

A subrecipient is an organization that receives funding from a grantee to carry out part of a program, while a contractor is an organization that provides goods or services to a federal award grantee as instructed and without any control over the program’s outcome.

The primary difference between the two is the level of control and responsibility that the grantee retains over the program. A subrecipient is typically given a significant level of autonomy and decision-making authority over the activities they are responsible for, and they are held accountable for meeting the objectives of the grant program. In contrast, a contractor is typically directed by the grantee on the specific work to be performed and how it is to be carried out. Contractors are responsible for delivering the agreed-upon goods or services, but they are not accountable for achieving the broader objectives of the grant program.

According to the Uniform Guidance1, while judgement is required, the following characteristics are indicative of either a Subrecipient or a Contractor relationship.

After determining a subrecipient relationship exists, the Uniform Guidance1 prescribes how subrecipients should be monitored by the ‘pass-through’ entity. This determination is particularly important as subrecipients must be in compliance with all Federal statutes, regulations, and the terms and conditions of the Federal award.

Monitoring Subrecipients

A successful relationship with a subrecipient begins with a good agreement between the two organizations. This will lay out the expectations for reporting, payment, audits, access, and other information needed to appropriately carry out subrecipient monitoring tasks. A risk evaluation of each subrecipient should be completed and documented in order to ensure the appropriate level of monitoring takes place throughout the award.

The risk assessment includes:

- Considering the subrecipient’s experience with similar awards.

- Reviewing financial and performance reports.

- Reviewing previous audits and the actions taken for audit findings.

- Considering the ability of the subrecipient personnel and systems.

- Current monitoring is already taking place related to other federal funding.

- Any additional tasks to ensure the risk of the subrecipient can be appropriately evaluated.

The risk assessment should be ongoing throughout the relationship with the subrecipient as new information is available.

Depending upon the risk assessment, your organization may be responsible for training the subrecipient, participating in on-site inspections of the operations, and potentially arranging agreed-upon-procedure engagements. While each subrecipient will have different requirements, the basic requirements of initial risk measurement and ongoing monitoring should be incorporated into a policy.

Subrecipient Monitoring Policy

Federal award grantees are encouraged to create and follow a subrecipient monitoring policy. This policy addresses the process and risk tolerance for selecting and monitoring subrecipients. From an accounting perspective, the accounting transactions related to this relationship, such as recording advances to subrecipients and the timing of expense liquidations, also need to be documented.

A typical accounting policy for recording subrecipient advances and the timing of expense liquidations may include the following:

- When the organization issues an advance payment to the subrecipient, the advance payment should be recorded as a receivable.

- Subrecipients have the responsibility of submitting expense reports to the organization. This begins the liquidation process of a subrecipient advance. A policy may define how often (i.e., monthly) and how soon after the period ends (i.e., within 15 days) these reports must be submitted. The methods to determine the accuracy of these reports and allowability of the expenses may also be defined within the policy. This expense report verification may involve reviewing the subrecipient's expense reports, supporting documentation, and verifying that the expenses are consistent with the terms of the award.

- When a subrecipient report has been received and verified, the advance liquidates and becomes an expense to the organization.

- Frequency of reconciliation between a subrecipient's advances and expense reports should be completed regularly with any discrepancies identified and resolved promptly.

- Define the award closure process with the subrecipient.

Overall, a sound accounting policy for subrecipient advances and expense liquidations is critical to ensuring compliance with the terms of the award, tracking outstanding advances, and timely reporting of expenses and funding requests.

Summary

Subrecipients play a crucial role in helping grantees fulfill their objectives, particularly in cases where the grantee lacks expertise or capacity. Understanding the difference between contractors and subrecipients is critical to ensure that the right type of relationship is established between the organizations. Successful relationships with subrecipients begin with a well-drafted agreement, a thorough risk assessment, and ongoing monitoring. Creating and following a subrecipient monitoring policy that addresses the selection, monitoring, and accounting transactions related to the subrecipient relationship is vital for good grant management. Ultimately, effective subrecipient monitoring is necessary to ensure the responsible and successful management of federal grant funds, and to protect the organization from potential risk.

1)Subrecipeint monitoring and management is discussed in detail within §200.331 - §200.333 of the Uniform Guidance.